A recently-published report updated our view on U.S. monetary policy under new Fed Chair Warsh and reiterated that the Fed is well behind the inflation curve.

While the FOMC finally acknowledged that policy rate hikes are now probable, the Fed is in no hurry and lower energy prices due to the U.S./Iran deal may give the Fed some (brief) breathing room. Critically, the Fed expects a rate hike or two to be sufficient to return inflation towards its target of 2%.

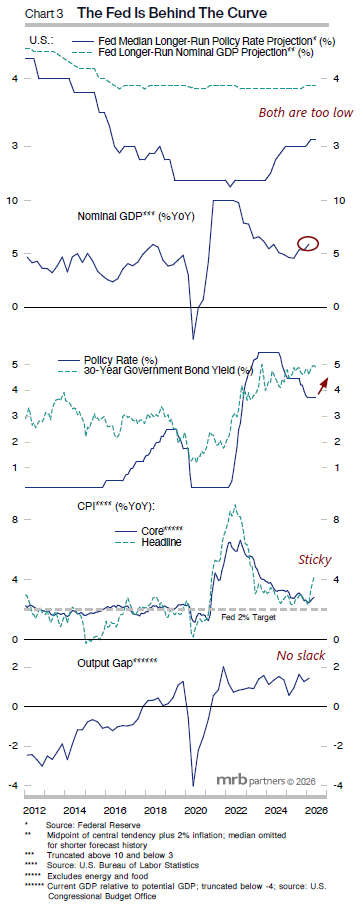

We have persistently disagreed with the Fed’s (low) forecast for future inflation. Moreover, we have also strongly disagreed with the Fed’s view that policy was ever restrictive this decade. Continued above-potential economic growth, inflation tracking well above the Fed’s target since early in the decade and ongoing rampant asset price inflation all add up to policy being too accommodative, for too long.

The Fed will ultimately have to lift rates by much more than it envisions and by more than the forward markets are discounting. We continue to position for higher U.S. and global government bond yields.