MRB Track Record

We find our use of flexible, but rigorous frameworks, our integrated global and multi-asset approach, and our formation of one cohesive viewpoint leads to a deeper and more holistic understanding of the forces at work in the global economy and financial markets. The result is stronger conviction, bolder calls, and more accurate investment strategy.

MRB has a strong track record of making accurate, non-consensus calls, and providing clients with a clear roadmap to help them set their investment strategy.

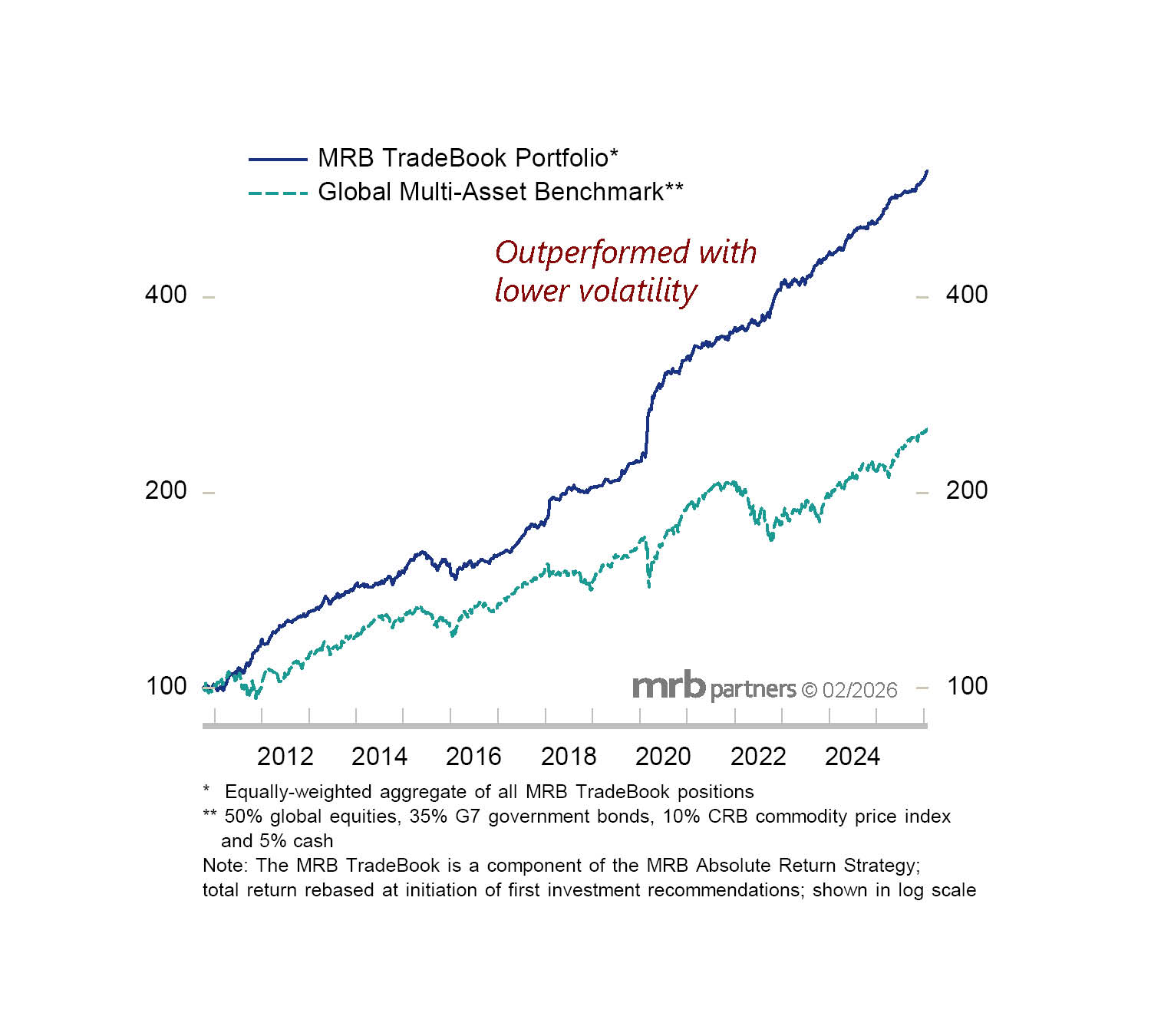

The MRB TradeBook Portfolio has outperformed the Global Multi-Asset Benchmark with lower volatility.

* Equally weighted aggregate of all MRB TradeBook positions

** 50% global equities, 35% G7 government bonds, 10% CRB commodity price index and 5% cash

Note: The MRB TradeBook is a component of the MRB Absolute Return Strategy; total return rebased at initiation of first investment recommendations; shown in log scale

The MRB TradeBook Portfolio