A just-published report updated our absolute return portfolio which remains mildly pro-growth, as risk-on is likely to persist until bond yields head north.

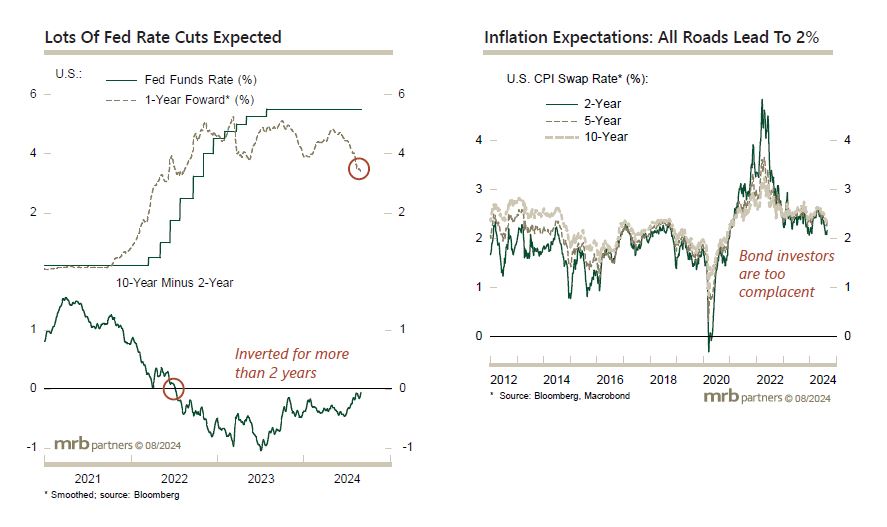

Financial markets have a way of frustrating the greatest number of investors when there is a strong consensus. To this end, after chronically and aggressively front-running the Fed rate-cutting cycle in recent years, perhaps U.S. Treasury yields could soon put in a bottom alongside the first Fed rate cut. While this would represent an unusual outcome, there have been many unusual features this cycle, not the least of which is that the economic and financial market environment that has typically been present at the start of a U.S. rate-cutting cycle does not currently exist.

Investors and the Fed remain complacent on the inflation outlook, still embracing the secular stagnation narrative from last decade that claims that all roads lead to 2% inflation. We disagree.

Net: there is limited downside for U.S. government bond yields unless a true recession develops, which we do not expect. Instead, the risks should skew to the upside for yields over time, despite the Fed’s dovish bias. We added a stop-short on U.S. Treasurys to capture the mispricing in the bond market and as a hedge against long equity positions.