A just-published report updated our regional equity strategy that has been complicated by the outsized weight of the U.S. in the global benchmark, the outsized weight of the technology sector in the U.S. and EM benchmarks, and the extraordinary recent performance of semiconductor stocks. We expect conventional cyclical factors to reassert their influence in regional equity performance over the next 6-12 months as the Middle East energy/commodity shock eases and the global economic expansion continues and, in fact, is likely to gain some strength.

Global equities will have support from improving corporate profits and accommodative monetary and fiscal policies, but a lot of good news is already discounted. The resumption of normal flows through the Strait of Hormuz should ultimately favor European and Asian economies and equity markets since they were most adversely affected by the earlier closure.

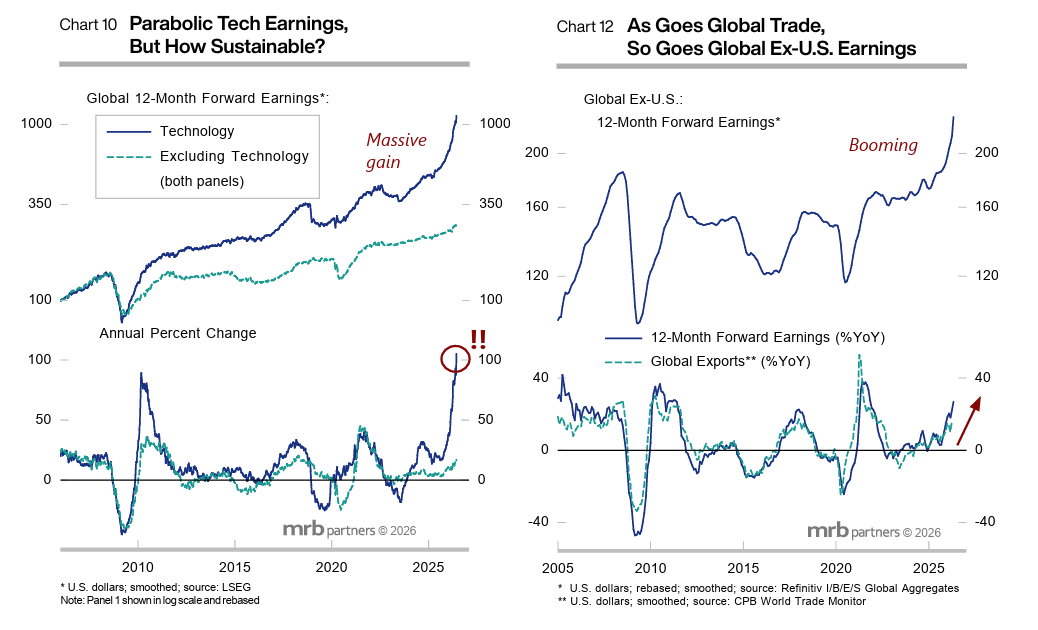

Diversification away from overbought tech is prudent and we recommend a mild underweight in the U.S. within a global equity portfolio.