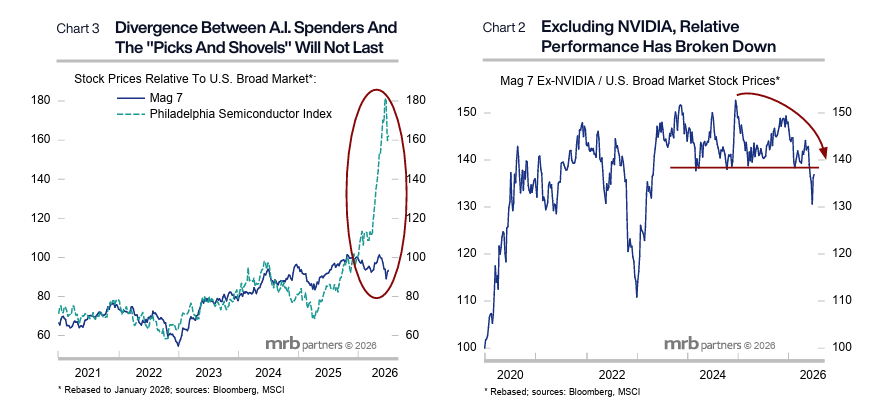

A just-published report examined the outlook for the previously high-flying Mag 7 stocks and the broader A.I. boom. Despite the continued enthusiasm for A.I., investors have recently punished the Mag 7 stocks due to the large capital expenditures of the hyperscalers on costly A.I. infrastructure, while rewarding the beneficiaries of this spending such as semiconductor and tech hardware stocks.

Given their growing external funding needs, it is risky to assume that hyperscalers will continue to double-down on capex if A.I. monetization does not soon pick up. Moreover, concerns about over-spending on A.I. will only increase speculation about a moderation in the pace of capex by the hyperscalers, thus triggering volatility in crowded semiconductor and tech hardware stocks. The late-1990s saw a similar divergence between the performance of telecom and communication equipment stocks that warned of the unwind of the Dot-Com bubble.

This tension should benefit select non-tech parts of the U.S. equity market including financials, health care, and the transportation and aerospace & defense components of the industrial sector.