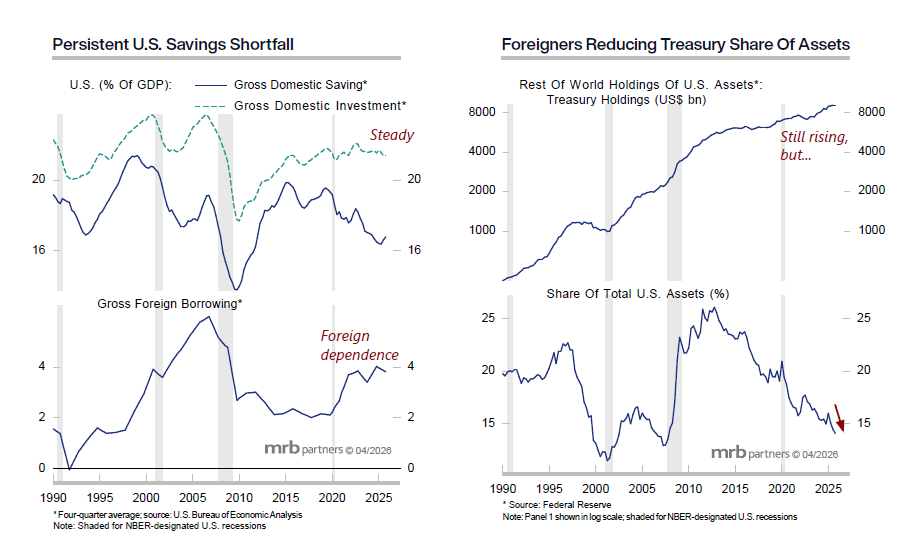

While investors have been almost exclusively focused on the war in the Middle East and the knock-on effect this has had on global energy prices and supplies, there remains a slow-moving but ever-worsening problem of increased demand from borrowers, both government and private sector, at a time of sticky DM inflation. The U.S. is at the forefront of this clash, especially as it has historically relied on foreign savers to finance its excess debt issuance.

In an MRB – The Macro Research Board report published last week “Increasing Pressure On U.S. Savings Adds To Treasury Risks” we examined this issue and highlighted the growing vulnerability in the Treasury market. The already high and rising U.S. federal budget deficit and increased corporate borrowing to finance capital spending alongside a declining domestic saving rate is a recipe for upward pressure on bond yields. The burden of financing the federal deficit will increasingly fall on domestic savers, with the Fed sidelined and foreign investors reducing their U.S. asset allocation to Treasurys.

Consequently, if the U.S. economic expansion persists, then domestic savers will be forced to increase their Treasury holdings, adding to the upward risks for U.S. Treasury yields in the year(s) ahead.