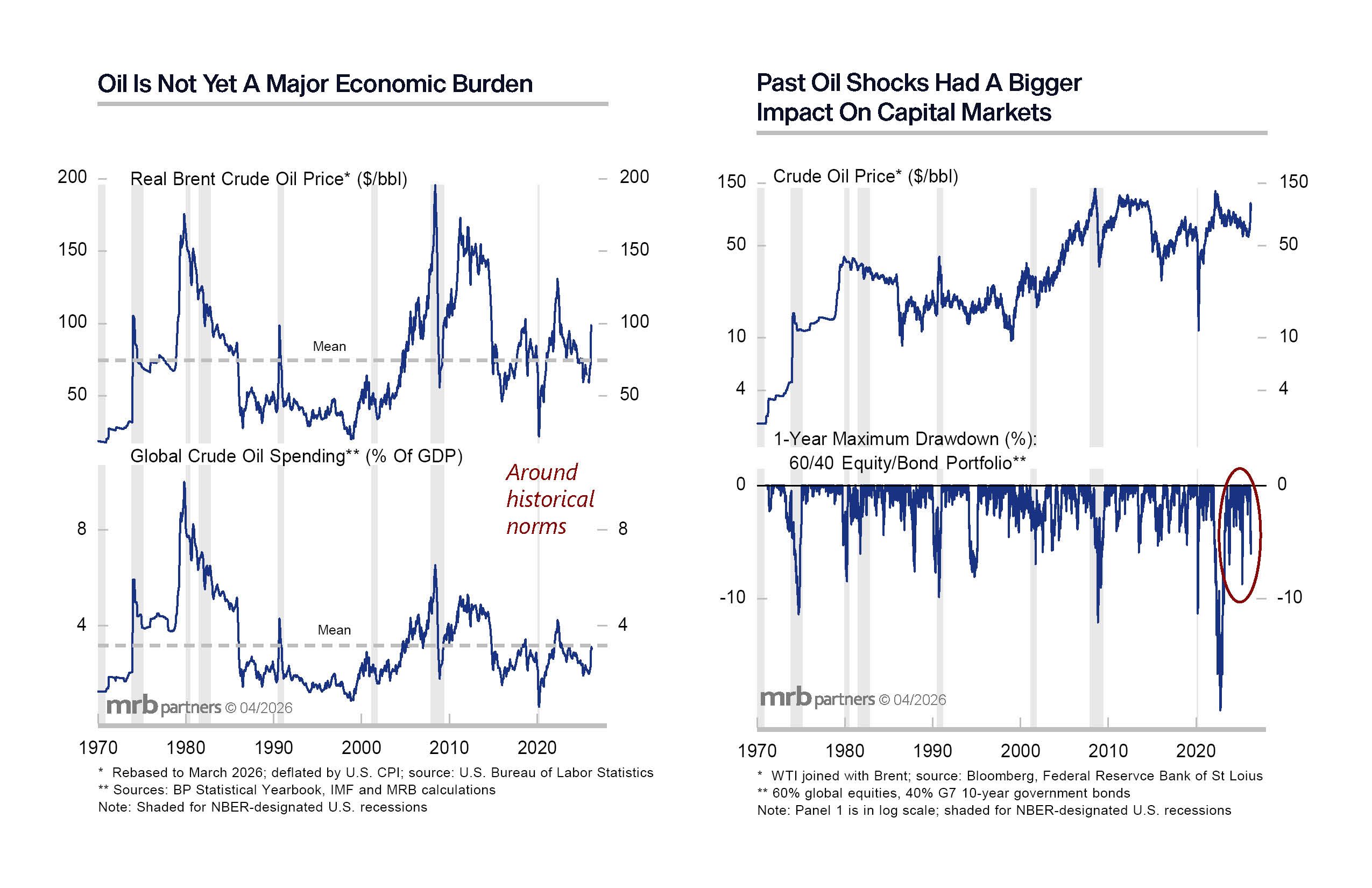

An MRB Report last week noted that while global oil prices have risen significantly since the war began, they remain well below past peaks in real terms. Likewise, global spending on crude oil relative to GDP is near its historical mean. Markets are likely to only factor in a global economic recession if Brent crude prices appeared likely to challenge the US$150/bbl level.

Nonetheless, past sharp increases in real oil prices have coincided with or triggered global equity bear markets or deep corrections. Several have also coincided with sizeable bond market losses, underscoring the potential threat to balanced portfolios if the war escalates materially or is drawn out. Handicapping the war/geopolitical outcome is difficult but we believe there is more downside if things go wrong, than upside if things go right.