A just-published report updated our multi-asset portfolio as we look out to the investment environment in 2025. The economic backdrop will be supportive of risk assets, but considerably lower returns on global equities loom and, by extension, balanced portfolios after this year’s strong gains. A moderate pro-growth portfolio tilt is appropriate for now, but there is the potential for sizable portfolio changes as the year progresses.

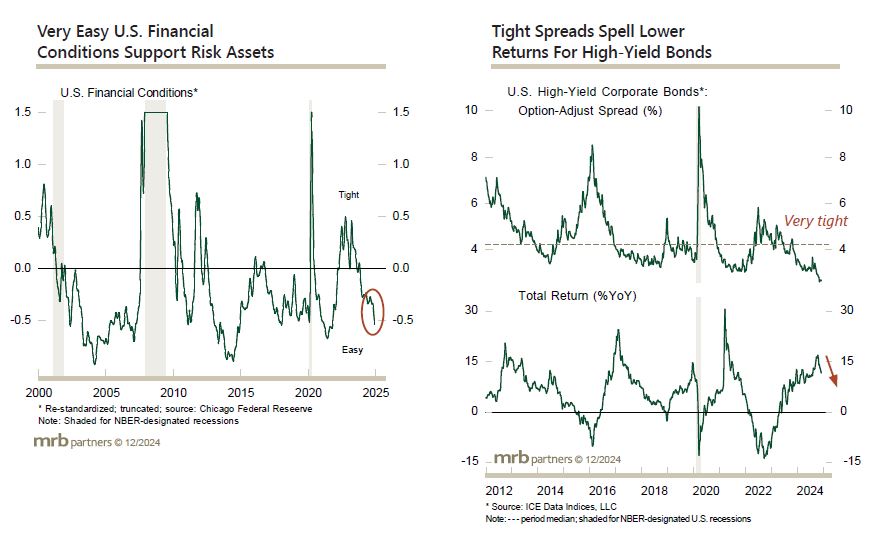

Greater market volatility will be driven by both heightened policy uncertainty as the next Trump Administration settles in (although we assume he will not jeopardize U.S. or global economic growth), and yet another upleg in global bond yields due to sticky DM inflation. U.S. 10-year yields will at least re-test the 5% level, and thus we remain underweight bonds in a multi-asset portfolio, and overweight inflation protection and credit within a fixed-income portfolio. However, credit will generate much lower returns given the starting point of historically tight spreads over government debt.

Rising corporate earnings should sustain the equity uptrend in the near run, but gains will be much more muted and volatile than in 2024. Risks will rise as bond yields eventually re-test 2023 highs. The risk-reward should eventually shift in favor of select non-U.S. equity markets, including emerging markets, Japan and the euro area.