A just-published report examined a number of timely investment issues, and updated our global investment strategy. The post-election stampede into all things U.S. has slowed, but investors remain wary of non-U.S. equity markets and currencies.

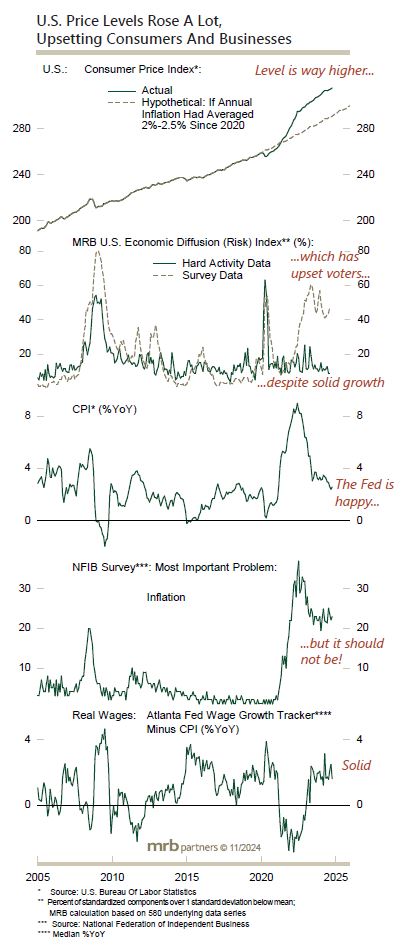

There have been many unique economic, inflation and market developments this decade. One recent notable divergence has been the rising trend in U.S. Treasury yields at a time when the Fed has been lowering interest rates. The widening gap between bullish hard U.S. economic data and very bearish survey measures is another unique development this decade. The hard data are still pointing to above-potential economic growth, and activity could even speed up with fresh monetary and fiscal stimulus in the pipeline.

There has also been a massive disagreement in the U.S. (and DM in general) regarding the issue of “inflation”. American voters are still angry with the huge increase in price levels this decade, which has far overshot pre-pandemic trends. Conversely, the Fed (and Treasury-bulls) believe that inflation has now been tamed, a view that we do not share. Rather, we expect sticky and above-target inflation to persist, as was reinforced with last week’s CPI report.

We remain underweight bonds within a multi-assert portfolio, and have several short positions in Treasurys, along with a long position in U.S. CPI Swap Rates.