A just-published report updated our global macro outlook and investment stance, highlighting the building risk of some digestion problems in the U.S. equity market. Last week’s turbulence also saw MRB recommend a number of new pair-trades to benefit from the evolving outlook.

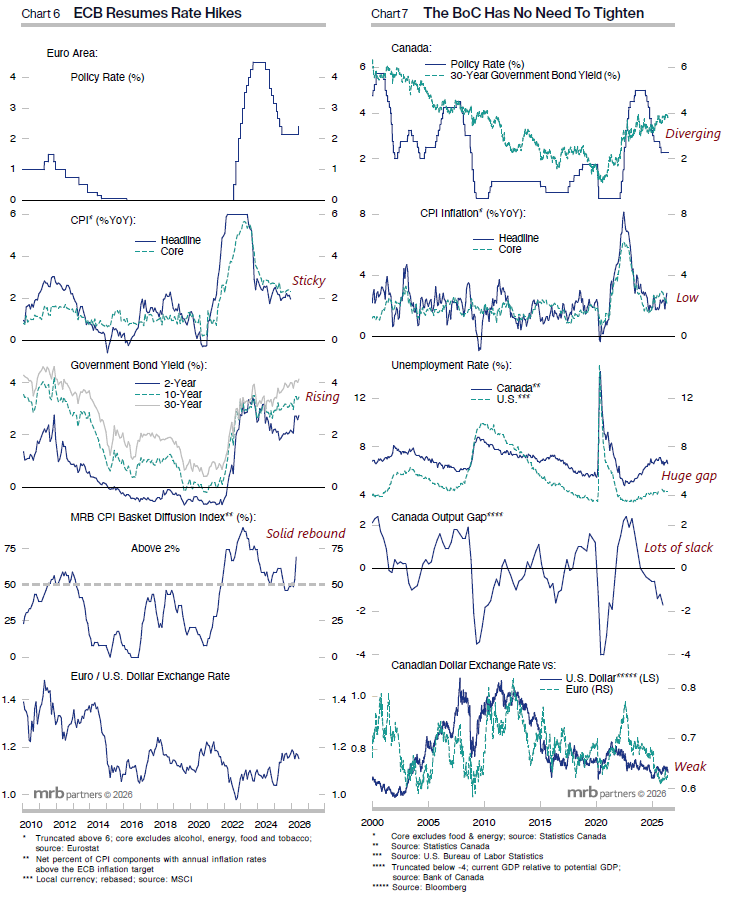

While concerns about a re-opening the Strait of Hormuz and the budding U.S. equity supply are the immediate threats, the greater (and much more durable) threat to the investment landscape is the likelihood of tighter DM monetary conditions and much higher government bond yields. Our research has highlighted the mounting pressures on most DM central banks, and indeed the ECB joined the rate-hiking “club” last week.

The Fed will continue to lag, despite having the greatest inflationary pressures. Regardless, the fed funds rate will ultimately head higher, far more so than is discounted.

The exception among the major DM central banks is the BoC, which left rates unchanged last week and has little pressure to hike despite the energy-related pop in headline inflation. As occurred in the U.S. and euro area last decade, easy monetary policies do not generate strong growth when an economy is de-leveraging, which is the case for the Canadian household sector.

Net: we remain bearish on bonds, even though yields may be briefly capped as investors struggle with various short-term risks. In the end, letting the inflation genie out of the bottle was a major error.