The macro environment remains supportive for risk assets, but there is an increasingly high bar for positive surprises. Investors should expect much more muted returns over the next 12 months and an increasing risk of a material setback in equities.

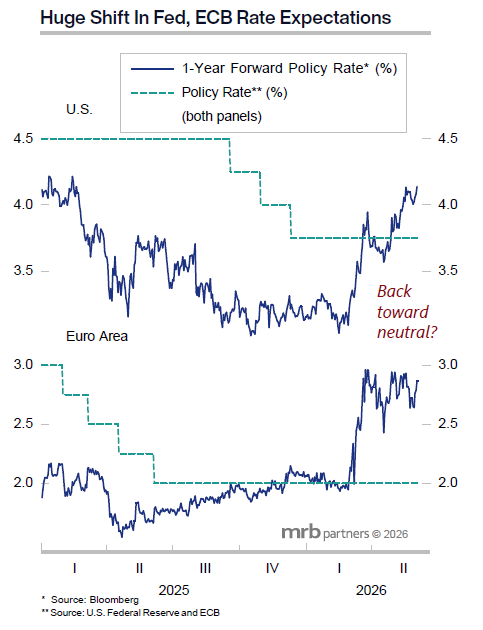

Our base-case scenario is that the Strait of Hormuz will soon begin to normalize, allowing global economic growth to improve. This, in turn, will sustain upward pressure on inflation and G7 government bond yields. The forward markets have already raced ahead and are discounting higher policy rates, which central banks, even the dovish Fed, will have to acknowledge.

Global corporate earnings are strong but rising at an unsustainable pace. This underscores the risk of disappointments ahead, at a time when bond yields have further upside. In turn, we recommend being selective in pro-growth positioning.