A just-published report updated how we expect U.S. monetary policy to evolve in the next 6 to 12 months. Needless to say we foresee a further unwinding of rate cut expectations and for the Fed to eventually be forced to reverse its dovish pivot.

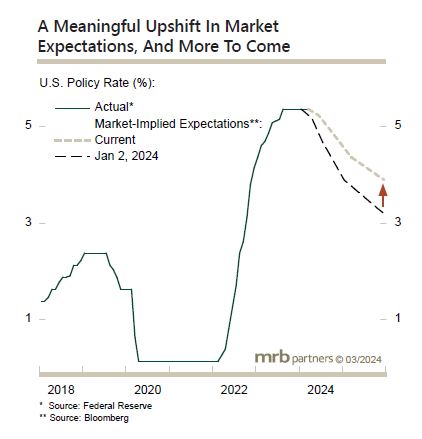

Despite a stronger growth and inflation outlook, the Fed stuck to its dovish bias at last week’s FOMC meeting, remaining firm on its signal to cut rates three times this year. Continued above-potential growth and the recent firming in underlying inflation means that the window for the Fed to cut rates this year has narrowed. There may still be a token reduction or two in the policy rate, but our view remains that the U.S. economy does not warrant rate cuts and the forward market will be forced to lift its policy rate path for next year.

The Goldilocks period for economic growth, risk assets and capped bond yields is still on, but sticky inflation will eventually trigger another upleg in bond yields and a bout of risk-off. We remain underweight bonds.