A just published report updated the MRB TradeBook which contains our absolute return positions. We have been pro-growth since last autumn, but recently tightened stops as the Goldilocks backdrop was expected to end once the rebound in bond yields gained momentum.

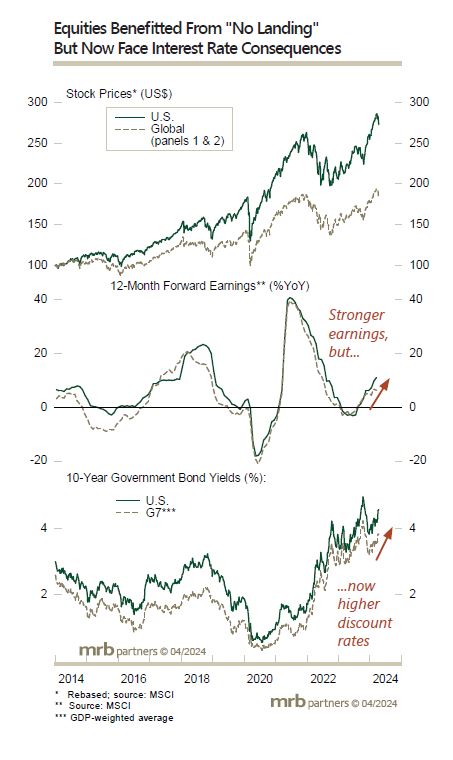

The Goldilocks environment began in 2023 Q4 with the Fed’s dovish pivot, which led to both firmer growth expectations and lower bond yields. It continued throughout 2024 Q1, as the upward revision to economic and earnings growth outpaced the rise in bond yields. We had expected Goldilocks to run into trouble when bond investors and/or central banks realized that they had been overly complacent on the inflation outlook, thereby driving bond yields higher. Such a transition is indeed underway.

The current level of U.S. and G7 bond yields is not yet crippling for the global economy. However, global equities (particularly the U.S. market) have already discounted solid economic and earnings growth, and will struggle as they adjust to higher-than-expected interest rates.

The end of Goldilocks does not necessarily mean a sustained equity bear market, but merely that the free lunch is over. The “buy everything rally” that began in late-October should give way to a more volatile trading environment, where selectivity becomes crucial.