Fed Chair Powell pivoted last autumn, claiming that monetary policy had become restrictive. This triggered a rush to discount aggressive rate cuts in 2024. The U.S. economy was in the midst of a powerful burst of growth during the second half of 2023, and thus risk asset markets also pivoted aggressively, with stock prices racing out to new highs and credit spreads narrowing significantly.

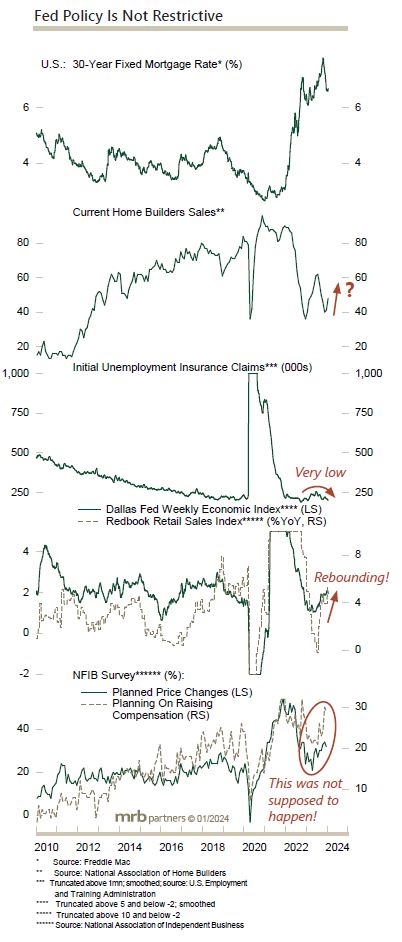

As just-published report updated our global investment strategy and addressed a number of topical issues, including Powell’s assertion that policy was restrictive. We found little evidence to support his claim. Even the one area that clearly had been weakening under the drag of higher borrowing rates, housing, is showing signs of life with both the Homebuilders’ survey and house sales rebounding. The overall economy has continued to grow at a rate well in excess of its long-run potential, and booming financial markets are certainly not signaling that liquidity is tight.

Net: the Fed may yet ease once or twice this year, even though the economic conditions that would warrant an easing in policy are not in place. Moreover, such conditions are not likely to develop given the fresh round of “stimulus” since late-October, via much lower borrowing rates. After being bearish on bonds in 2021-2023, we turned neutral last autumn as bond yields briefly hit undervalued levels. We now anticipate returning to an underweight stance on bonds within a multi-asset portfolio, perhaps shortly – stay tuned.